Date: 06/02/2024

iPhone Hits Record 50% Revenue Share on US, India and Emerging Markets; China Risks Remain

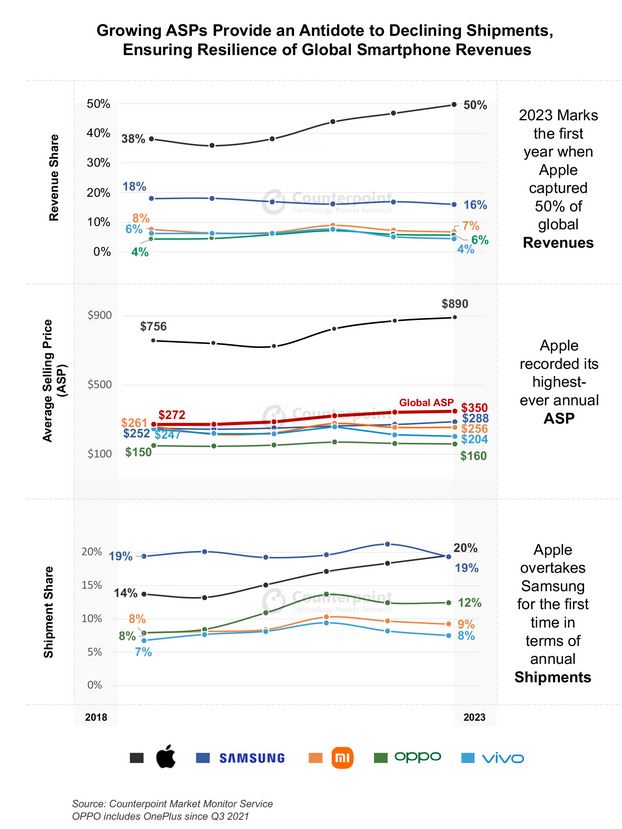

Continued strength in premium and ultra-premium increase Apples ASP by 2% YoY to a record $890.

Driven by ASP growth, Apples 2023 iPhone revenue reached a record $203 billion

Apple also overtook Samsung to become the number one brand globally in shipment share on an annual basis for the first time.

Total market shipments declined by 4% in 2023 driven by macroeconomic challenges, especially in the first half of the year.

Samsungs broader portfolio exposed it to lower-end segment weakness which saw both revenues and shipments decline.

Value (vs volumes) and ASPs are the key metrics to watch, as OEMs continue to pivot upwards thanks to foldables and features like GenAI in flagship models.

Global smartphone market revenues declined by 2% to a little under $410 billion in 2023 compared with a 4% decline in shipments to 1.17 billion units. This is thanks to a 2% growth in global smartphone ASPs which touched $350 for the first time. Apple led the market with a 50% share of global smartphone revenues, its highest-ever for a full year. This contributed to the ongoing premiumization trend with one in every four smartphones shipped in 2023 wholesaling for more than $600. Consequently, while the non-premium segments experienced double-digit declines, premium smartphone shipments grew by 8% driven by foldables, features like GenAI, and, of course, Apple.

Commenting on Apples performance in 2023, Research Director Jeff Fieldhack noted, Apple displaced Samsung as the biggest player in shipments for the first time in a full year. While the US made the biggest volume contribution to Apples growth, it also received a major boost through double digit growth in emerging markets including India, Caribbean and Latin America (CALA) and Middle East and Africa (MEA). This growth offset any challenges Apple may have faced in China due to the resurgence of Huawei. With an accompanying ASP growth of 2%, it can be seen to be in a revenue super cycle, buoyed by its ecosystem stickiness coupled with the premiumization trend, crossing an annual revenue of $200 billion.

Elaborating on Apples performance in China, Senior Analyst Ivan Lam said, The positive emerging market offset is a welcome news, but China remains a slight concern. The markets recovering but Apple is facing competition from a resurgent Huawei in the premium segment and multiple China OEMs digging into iPhone 13 and 14 volumes. Well see whether Apple will get aggressive on pricing over the critical weeks before Chinese New Year and how this correlates to volume increases.

Samsung, the longstanding market leader in terms of shipments suffered setbacks on multiple fronts, ceded some share in premium markets to Apple. Its mid-tier phones also faced increasing competition from Chinese OEMs including Xiaomi and vivo in markets such as India. Its lower-end devices were challenged by Transsion Group in MEA and South East Asia (SEA).

Major Chinese OEMs, other than Huawei and HONOR, suffered shipment as well as revenue declines in 2023. Among the top five brands, vivo suffered a 16% revenue and a 12% shipment decline as a result of relatively weak performance in Europe and the timing of its flagship launch. OPPOs* revenue and shipment declines stood at 9% each. A steeper decline was prevented thanks to the growth of OnePlus within OPPO Group. OPPOs* challenges in the lucrative European market may be improving since it has signed a 5G patent cross-licensing agreement with Nokia.

Overall global smartphone ASPs are also likely to continue their upward journey with vendors, carriers, and retailers preferring to sell higher-end models. While on the demand side, backed by better financing options, consumers have also shown greater willingness to spend more for longer lasting devices. The resurgence of Huawei in China is also likely to contribute to ASP growth.

Source: Counterpoint

Tweet Follow @ecewire